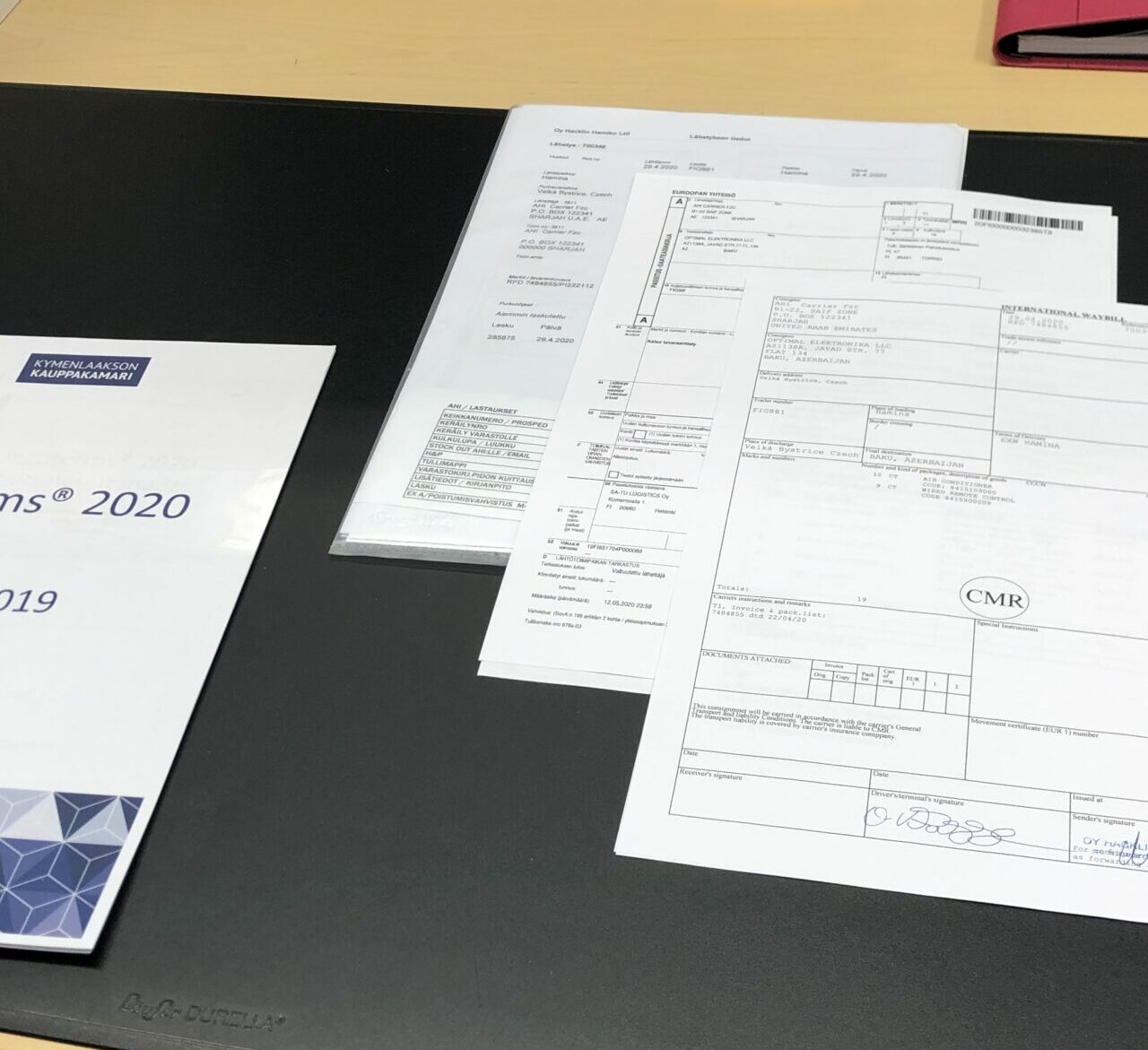

Incoterms, or delivery terms, are trading conditions of the International Chamber of Commerce (ICC), which define the responsibilities of the buyer and seller regarding the delivery, the goods and costs.

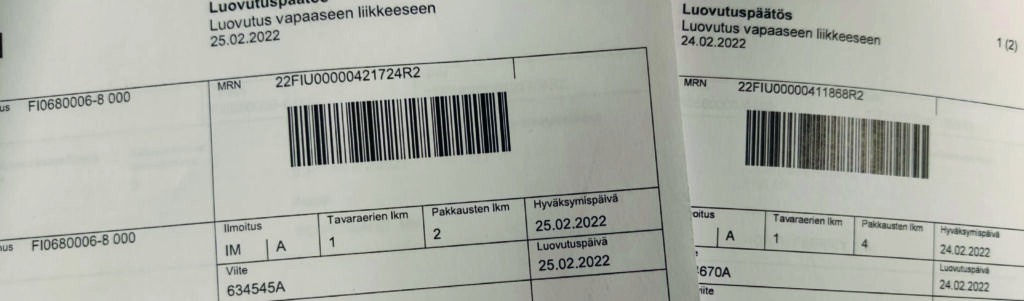

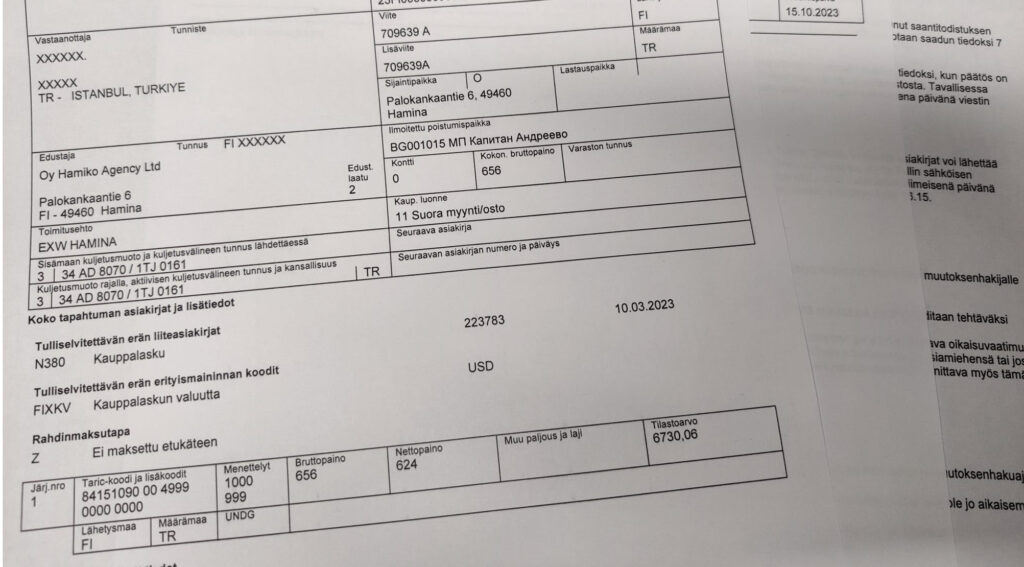

The delivery term should be indicated at the trade invoice used for issuing the customs declaration.

Incoterms 2020

All modes of transport

EXW: Ex Works; Collected from the seller

FCA: Free Carrier; Seller delivers to the carrier

CPT: Carriage Paid To; Transport paid

CIP: Carriage and Insurance paid to; Transport and insurance paid

DAP: Delivered at Place; Delivered to place of destination

DDP: Delivered Duty Paid; Delivered cleared for import

DPU: Delivered at Place Unloaded

Sea and Inland Waterway Transport Only:

FAS: Free Alongside Ship; Placed alongside the vessel

FOB: Free On Board; Delivered on-board the vessel

CFR: Cost and Freight; Costs and freight paid

CIF: Cost, Insurance and Freight; The costs, insurance and freight are paid

Adding the cost of freight, insurance and related costs to the trade price:

EXW: The buyer bears all costs of freight, insurance and related costs from the place stipulated in the terms of delivery. These costs are added to the trade price to the EU border.

FCA: The buyer bears all costs of freight, insurance and related costs from the place stipulated in the terms of delivery. These costs are added to the trade price to the EU border.

CPT: The seller pays the freight and related costs to the stipulated place of destination. These are already included in the trade price, i.e. they are not added. The buyer pays the insurance, which is added to the trade price.

CIP: The seller pays the freight, insurance and related costs to the destination stipulated in the terms of delivery. These costs are included in the trade price and no costs are added.

DAP: The seller pays the freight, insurance and related costs to the destination stipulated in the terms of delivery. These costs are included in the trade price and no costs are added.

DDP: The seller pays the freight, insurance and customs formalities to the destination stipulated in the terms of delivery. Freight and insurance costs are included in the trade price and no costs are added. Import taxes levied within the Union can be subtracted from the trade price.

DPU: The seller pays the freight, insurance and related costs to the place of unloading specified in the terms of delivery. These costs are included in the trade price and no costs are added.

FAS: The buyer bears all costs of freight, insurance and related costs from the place (alongside the ship) stipulated in the terms of delivery and onwards. These costs are added to the trade price to the EU border.

FOB: The buyer bears all costs of freight, insurance and related costs from the destination stipulated in the terms of delivery and onwards. These costs are added to the trade price to the EU border.

CFR: The seller pays the freight and related costs to the named port of destination stipulated in the terms of delivery. These costs are already included in the trade price and are not added to the taxable amount. The buyer pays the insurance costs, which are added to the trade price.

CIF: The seller pays the freight, insurance and related costs to the named port of destination stipulated in the terms of delivery. These costs are included in the trade price and no costs are added.

Any question? Contact us!